When it comes to reverse mortgages, many people ask how the loan works. The product is not understood by most homeowners so it’s understandable they would be curious about the math behind this unique type of mortgage.

This article will explain how interest is calculated on a reverse mortgage in Canada.

Key Takeaways:

- Reverse mortgages allow homeowners over 55 years to tap into their home equity without monthly payments.

- Interest on a reverse mortgage is calculated on the actual amount borrowed, not the amount you may be eligible for.

- Interest is compounded semi-annually for fixed interest rates and monthly for variable interest rates.

- Both fixed and variable rate reverse mortgages calculate and charge interest on a daily basis.

What is a Reverse Mortgage?

A reverse mortgage is a loan that allows homeowners over the age of 55 to tap into their home equity without having to make any monthly mortgage payments. The loan, along with the accumulated interest, is repaid when the homeowner sells their home, moves out, or passes away.

For more information on reverse mortgages, check out our comprehensive guide to reverse mortgages.

How to Calculate Interest on a Reverse Mortgage

The interest on a reverse mortgage is calculated based on the amount you actually borrow, not the maximum limit you could borrow. To find out what your maximum loan limit could be, try our reverse mortgage calculator that can be used without providing any personal information.

The interest calculations on a reverse mortgage will depend on whether you have a fixed rate reverse mortgage or a variable rate reverse mortgage.

What is a Fixed Rate Reverse Mortgage?

A fixed rate reverse mortgage is a loan whose interest rate remains the same for its entire term. This means your interest costs will be predictable over the term of the mortgage.

What is a Variable Rate Reverse Mortgage?

A variable rate reverse mortgage, on the other hand, is a loan whose interest rate can change over time. The variable rate on a reverse mortgage will be based on the lender’s “prime rate” plus a certain extra amount (known as the “spread”).

The lender’s prime rate is itself based on the Bank of Canada’s prime rate. This means the interest rate on your variable rate reverse mortgage will change during its term if the Bank of Canada changes its prime rate.

What is the Compounding Period of a Reverse Mortgage?

If you have a fixed rate reverse mortgage, your mortgage will compound semi-annually (every 6 months). If you have a variable rate reverse mortgage, your mortgage will compound monthly.

What is Compounding?

Compounding is the process of adding the interest accrued on a loan to the principal balance, which then becomes the number you use for future interest calculations. We often refer to compounding as charging “interest on interest”.

Compounding interest is different from simple interest, where interest is calculated only on the original principal amount. Here's a simple table to illustrate the difference between compound interest and simple interest using a loan amount of $100,000 and an interest rate of 5%:

As you can see in this table, with compounding interest, the amount of interest accrued each period increases (from $5000 to $5262) because it's calculated on a larger principal amount every period.

With simple interest, the interest amount stays the same at $5000.

How Often is Interest Calculated on a Reverse Mortgage?

Both fixed and variable rate reverse mortgages calculate and charge interest on a daily basis. This is similar to how credit cards calculate interest.

How is Interest Calculated on a Fixed Rate Reverse Mortgage?

Let’s take everything we’ve discussed and put it together to see how interest is calculated on a fixed rate reverse mortgage. Let's assume you borrow a lump sum of $100,000 for a 1-year term with a fixed rate reverse mortgage, and the annual interest rate is 4.89%.

Step 1: Since reverse mortgages charge interest on a daily basis, we need to convert our annual interest rate of 4.89% into a daily interest rate. We do this by dividing our annual interest rate by 360 days (we’ll use 360 days for easier calculations): 4.89% / 360 days = 0.01358% per day.

Step 2: Calculate the daily interest amount using the daily interest rate we just calculated in Step 1: $100,000 (the amount you borrowed) x 0.01358% = $13.58 interest per day.

Step 3: Calculate the interest amount for the compound period using the daily interest amount calculated in Step 2: Since we are compounding semi-annually (or every 6 months) we need to multiple the daily interest amount by the number of days in the compound period (we’ll work with 180 days for simplicity): $13.58 x 180 days = $2,444.40 interest for the first compound period. This interest amount is then added to the principal, and will be used to calculate the interest amount for the next compounding period.

Here's a table for this fixed rate reverse mortgage scenario:

How is Interest Calculated on a Variable Rate Reverse Mortgage in Canada?

Now let’s do the same thing to see interest is calculated on a variable rate reverse mortgage. Suppose you decide to borrow $100,000 for a 1-year term with a variable rate reverse mortgage. The initial interest rate is set at P+3%, where P is the prime rate, which is currently 6.7%. This gives you an initial interest rate of 9.7 (For simplicity, let's assume that each month has 30 days and that the prime rate increases by 0.25% at the end of month 6)

Step 1: Since reverse mortgages charge interest on a daily basis, we need to convert our annual interest rate of 9.7% into a daily interest rate. We do this by dividing our annual interest rate by 360 days (instead of 365 days for simplicity): 9.70% / 360 days = 0.02694% per day.

Step 2: Calculate the daily interest amount using the daily interest rate we calculated in Step 1: $100,000 (the amount you borrowed) x 0.02694% = $26.94 interest per day.

Step 3: Calculate the interest amount for the compound period using the daily interest amount calculated in Step 2: Since we are compounding monthly, or every 30 days, we need to multiple the daily interest amount by the number of days in the compound period: $26.94 x 30 days = $808.20 interest for the first compound period. This interest amount is then added to the principal, and will be used to calculate the interest amount for the next compounding period.

Remember, we assumed the prime rate increases by 0.25% at the end of month 6. This means your new interest rate in month 7 and afterwards is 9.95% (we get this by adding P+3%+0.25% or 6.7%+3%+0.25%). With the rate increase, our daily interest rate in month 7 and afterwards becomes: 9.95% / 360 days = 0.02764% per day

Here is a table that shows how the interest calculations would work out for a variable rate reverse mortgage:

As you can see, the variable rate reverse mortgage interest rate calculations can be a bit more complex due to the changing interest rate. Variable rate reverse mortgages can potentially offer savings if the prime rate decreases during the term of your mortgage. Unfortunately if interest rates are rising (as they currently are), then a variable rate reverse mortgage will not be very attractive.

As always, it's important to consult with a financial advisor to understand the potential risks and benefits of variable rate mortgages.

Why are Reverse Mortgage Interest Rates High?

Reverse mortgage rates are typically higher than regular mortgage rates because lenders are not receiving monthly payments from borrowers. According to HomeEquity Bank, since the lender is not repaid for a long period of time, they cannot access normal mortgage funding sources and must pay a premium in the capital markets for funding CHIP reverse mortgages.

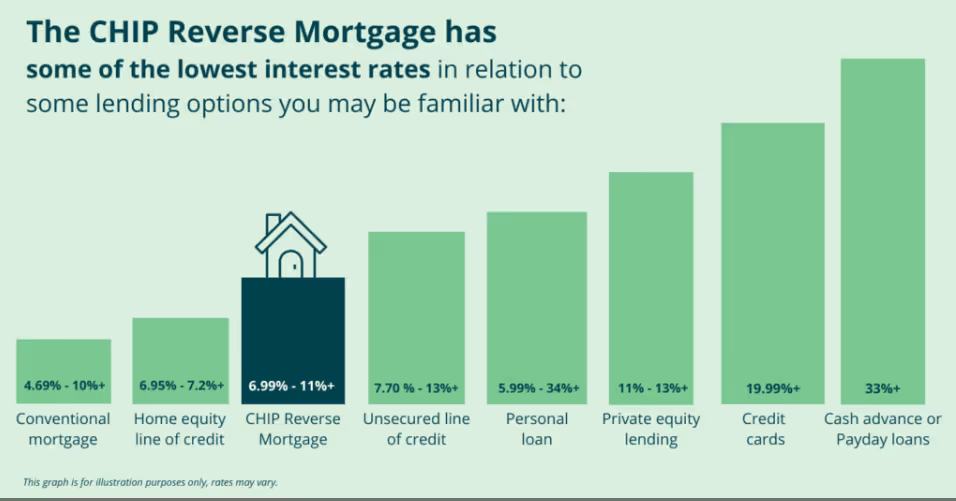

While reverse mortgage interest rates are higher than traditional mortgages, they are lower than many other loan options homeowners may be familiar with such as credit cards, personal loans and payday loans.

Conclusion

Understanding how interest is calculated on a reverse mortgage in Canada can help you make informed decisions about your financial future. But if you don’t understand the math, speak to a reverse mortgage expert who can provide you with tables showing all the interest charges already calculated for you. You do not need to do these calculations yourself!

FAQ

Q1. How are monthly payments calculated on a reverse mortgage in Canada?

A. Monthly payments are not calculated on a reverse mortgage since borrowers do not need to make monthly payments to the lender. Lenders do, however, calculate interest monthly and add it to the loan which makes the mortgage balance increase over time.

Q2. How does Equitable Bank calculate interest on its Flex reverse mortgage?

A. Both Equitable Bank and HomeEquity Bank calculate interest in the same way. Other regional reverse mortgage lenders may calculate interest differently so you should consult with a reverse mortgage advisor.