When is the Best Age to Get a Reverse Mortgage in Canada?

"I’ve been thinking about a reverse mortgage, but I’m just not sure if now is the right time. What do you think?"

This is a question I hear often from clients.

And I get it: financial freedom is part of the retirement dream and everybody wants to live a worry-free retirement. On the flip side, nobody wants to make a financial mistake in retirement.

And so they focus on this timing question. WHEN should a person have a reverse mortgage?

In this article, we’ll look at this question and see if there really is a best age to get a reverse mortgage.

Understanding Reverse Mortgages

As always, it helps to make sure we all know the basics of reverse mortgages.

A reverse mortgage is a financial product that allows Canadian homeowners aged 55 and older to borrow money against the equity in their homes without selling the property.

Unlike a traditional mortgage, there are no monthly payments. The loan is repaid when you sell the house, move out, or pass away.

In Canada, two popular reverse mortgage products are the CHIP Reverse Mortgage provided by HomeEquity Bank and the Flex Reverse Mortgage provided by Equitable Bank.

Learn more:

Which Lenders Offer Reverse Mortgages in Canada?

The Ultimate Guide to CHIP Reverse Mortgages

Both options are designed to help retirees access their home equity while continuing to live in their homes. The amount you can borrow depends on several factors, including your age, the value of your home, and current interest rates.

Using a reverse mortgage calculator can provide you with a personalized estimate, helping you understand how much equity you might be able to access based on your specific situation.

Learn more:

Our Review of Online Reverse Mortgage Calculators

Methodology: Basis of the Analysis

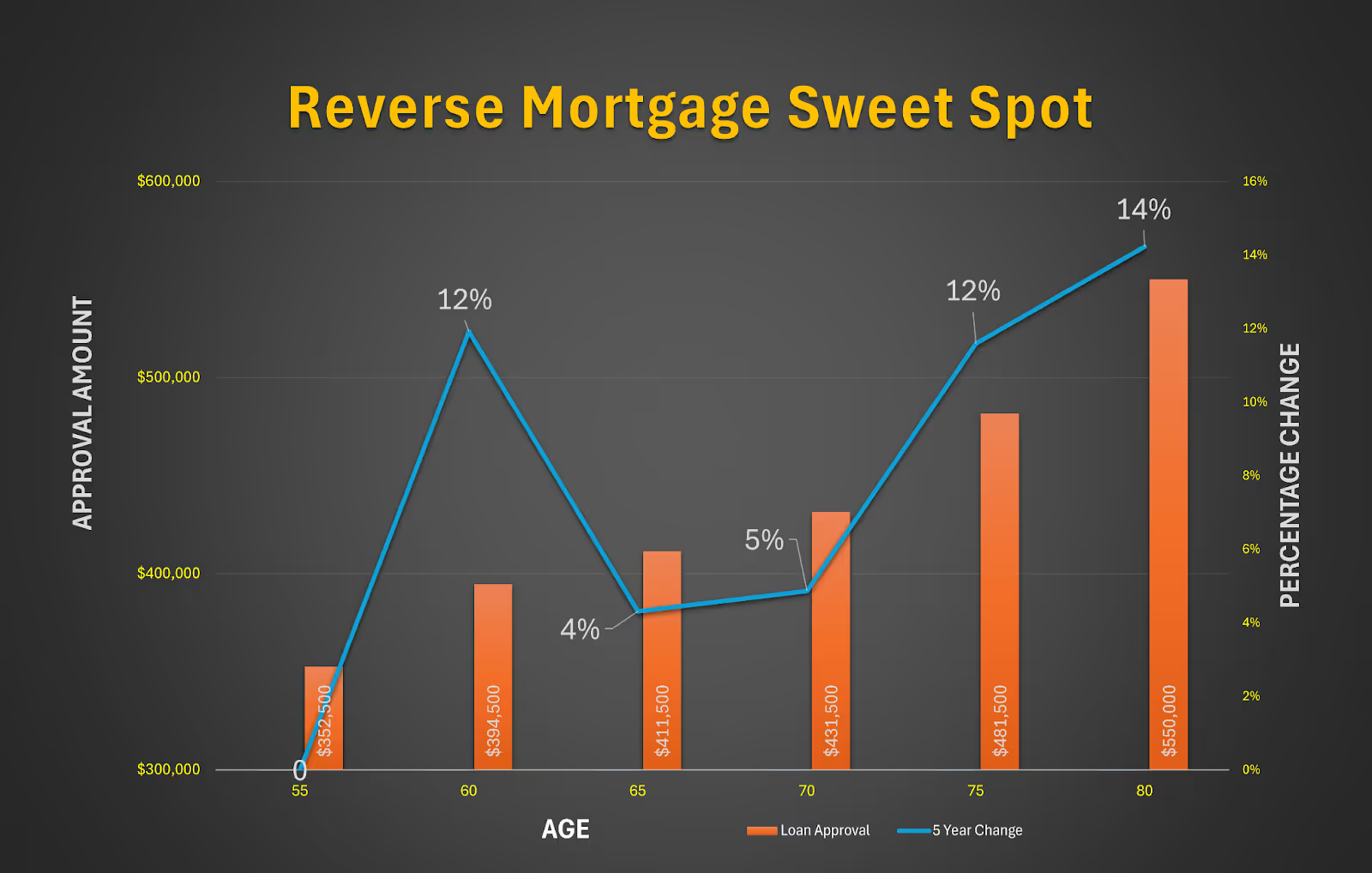

For the purpose of this article, I decided to look at reverse mortgage approvals for a single male living in a single family home worth $1,000,000 in a suburb of Ontario. I generated reverse mortgage quotes based on ages ranging from 55 to 80 and compared the changes year over year.

By doing this, I was able to see how much approvals increased year-over-year and whether there were certain ages that stood out for getting higher approvals (relatively speaking) than others.

It’s important to note that results can vary if different locations or property values are used. Additionally, including a second homeowner of a different age could significantly alter the outcomes.

The Best Ages to Get a Reverse Mortgage

There are two key age ranges—or "sweet spots"—where reverse mortgage approvals see significant year-over-year increases. These sweet spots occur between the ages of 55-60 and 70-75.

During these periods, the increase in loan approval amounts is substantial, making them ideal times to consider taking out a reverse mortgage.

Understanding the significance of these sweet spots can help you make an informed decision about when to access your home equity.

Outside of these periods, the increases in approval amounts tend to be nominal, which may not justify the wait if you need funds sooner.

The results are summarized in the following chart:

From this chart, you can see that the loan approvals increase from 4% to 12% as you move from one age group to the other.

With this in mind, I would say it makes sense to wait until you are 60 to get a reverse mortgage rather than getting one at the age of 55 because your approval amount will increase by 12%.

The same view would apply if you are 70—wait until you are 75 because your loan approval will increase by 12% as well.

For all other ages, I wouldn’t wait because your loan approval will not increase in a significant manner, typically 4% over a 5 year period.

But life isn’t that simple, is it? I don’t think you can answer our question without looking at context, or more specifically, the needs of the borrowers.

Two Types of Borrowers

If we are going to consider the needs of a borrower when considering the best age to get a reverse mortgage, then it makes sense to consider 2 types of borrowers.

Type 1: Mortgage-Free and Comfortable in Retirement

This type of borrower is mortgage-free and living comfortably on their retirement income. They have no immediate need for additional funds and can afford to wait to maximize their home equity.

For these borrowers, the best strategy is often to wait as long as possible, ideally until the second sweet spot between ages 70-75.

By waiting, they can benefit from significant year-over-year increases in loan approval amounts and preserve as much equity as possible for future needs or for their heirs.

Type 2: Carrying a Mortgage and Struggling in Retirement

This type of borrower still has a mortgage and other debts and finds it challenging to maintain a comfortable lifestyle on their retirement income.

For these borrowers, waiting until the ages of 70-75 might not be the best option.

The financial pressure they face makes it more beneficial to access a reverse mortgage during the first sweet spot, between ages 55-60.

By taking action during this period, they can immediately improve their quality of life, reduce financial stress, and eliminate mortgage payments, even if it means accessing a smaller loan amount compared to waiting until later.

Should You Wait or Act Now?

Type 1 Borrowers: Pros and Cons of Waiting

Pros of Waiting:

- Maximized Equity: By waiting until the second sweet spot or later, Type 1 borrowers can take advantage of significant increases in loan approval amounts, preserving more equity for future needs or for their heirs.

- Financial Flexibility: With no immediate need for funds, these borrowers can afford to wait and see how their financial situation evolves, potentially accessing a larger amount when they need it.

Cons of Waiting:

- Uncertainty: Life can be unpredictable, and waiting too long might result in unforeseen expenses or needs that could require accessing funds sooner.

- Opportunity Cost: By not accessing the funds earlier, these borrowers might miss out on opportunities to enhance their lifestyle or invest in other areas of their retirement.

Type 2 Borrowers: Pros and Cons of Acting Early

Pros of Acting Early:

- Immediate Relief: Accessing a reverse mortgage during the first sweet spot can provide immediate financial relief, improving quality of life and reducing the burden of mortgage payments and other debts.

- Stability: For borrowers struggling to maintain their lifestyle, acting early can provide the stability they need to enjoy their retirement without the stress of financial uncertainty.

Cons of Acting Early:**

- Interest Accumulation: Taking out a reverse mortgage at a younger age means that interest will accumulate over a longer period, potentially reducing the amount of equity available later in life.

- Potentially Lower Loan Amount: By accessing funds during the first sweet spot, borrowers might receive a smaller loan amount compared to waiting until the second sweet spot.

Real-Life Scenarios and Case Studies

Case Study 1: A Mortgage-Free Retiree (Type 1)

Janet (name changed for privacy reasons) is a 72-year-old widow living in Ontario. She has been mortgage-free for several years and is comfortably living on her retirement income.

We recognized that Jane didn’t need immediate access to her home equity and so advised her to wait until the second sweet spot (ages 70-75) to take out a reverse mortgage.

By waiting, she was able to secure a larger loan amount, which she plans to use for future healthcare needs and to leave as an early inheritance for her children.

Case Study 2: A Retiree with a Mortgage (Type 2)

Bill (name changed for privacy reasons) is a 58-year-old retiree who still carries a mortgage and finds it challenging to manage his finances.

We could see that Bill was financially stressed and not enjoying a high quality of life. As a result, we advised Bill to take out a reverse mortgage during the first sweet spot (ages 55-60) rather than to wait.

This allowed him to pay off his remaining mortgage, eliminate monthly payments, and significantly reduce his financial stress, enabling him to enjoy his retirement years more comfortably.

Conclusion

Deciding the best age to get a reverse mortgage has to depend on your individual circumstances and financial goals.

For mortgage-free retirees who are comfortably managing their finances, waiting until the second sweet spot—or even later—can maximize their equity and provide larger loan amounts.

For those carrying a mortgage and struggling to maintain their lifestyle, accessing a reverse mortgage during the first sweet spot can offer immediate financial relief and improve quality of life.

Ultimately, reverse mortgages should be viewed as a lifestyle product designed to enhance your retirement years.

The decision of when to access your home equity should align with your personal needs, whether that means waiting for a better financial result or acting sooner to relieve financial pressure.

Unsure About When to Get a Reverse Mortgage? Contact RetireBetter

If you’re considering a reverse mortgage, it’s important to understand that this is more than just a financial decision—it’s about improving your quality of life.

At RetireBetter, we understand that every homeowner’s situation is unique. Whether you’re ready to access funds now or are considering waiting, our experts are here to help you make the best decision for your circumstances.

And of course, it’s OK if you’re not sure how to deal with your specific situation. Contact RetireBetter to discuss your options, including our unique solutions like bundled reverse mortgages.

You can also use our reverse mortgage calculator to get a personalized estimate, and take the first step toward a more secure and fulfilling retirement.