When considering any kind of home loan, such as a reverse mortgage, it’s natural to give consideration to how it can impact your family and the inheritance they receive.

At RetireBetter, we understand many people are attracted to the benefits of a reverse mortgage but are concerned about its disadvantages. In particular, we know homeowners worry that a reverse mortgage will prevent other family members from receiving an inheritance.

In this article, we'll explore reverse mortgages, dispel common misconceptions, and learn about the impact a reverse mortgage can have on your heirs.

Understanding Reverse Mortgages

A reverse mortgage is a unique financial tool available to homeowners aged 55 and older, allowing them to tap into their home equity while maintaining ownership of their property.

Unlike a traditional mortgage, where borrowers make monthly payments to the lender, a reverse mortgage does not require homeowners to make any payments for the life of the loan.

We’ve written a great deal about reverse mortgages and you can visit our site to learn more about the pros and cons of a reverse mortgage.

Preserving Your Family' Inheritance

It's natural to have concerns about the impact of a reverse mortgage on your family’s inheritance. One common misconception is that your family will have to deal with your debt after your passing.

However, the truth is that reverse mortgages in Canada are non-recourse loans. This means that the lender cannot pursue your heirs or your estate for any shortfall between the loan balance and the home's value.

Estate planning strategies with reverse mortgages

With a reverse mortgage, you can tap into your home's equity while still retaining ownership. This opens up a world of possibilities for estate planning. Here are some powerful strategies to consider:

Preserving Your Family’s Investments: When you get a reverse mortgage, you are able to use your own home’s equity and live with financial independence. This ensures that you are not dependent on your family for your lifestyle, medical expenses, or any other type of expenses. When you do not depend on your family, they save their money which they can then invest themselves. This allows your heirs to create a diverse retirement portfolio for themselves without still allowing you to preserve your own retirement lifestyle.

Preserving Your Legacy: With careful planning, a reverse mortgage can help you preserve your wealth and create a lasting legacy for future generations. How?

Depending on your circumstances, you can use your reverse mortgage to make new investments. If you make suitable investments, with time your portfolio will only grow.

So, when it’s time to leave the house, sell it, or if you pass away, your heirs will not only have the home to pay the lender, but might also have more from your strategic investments. This way, you can ensure you leave a legacy for your heirs.

Remember, consulting with professionals specializing in estate planning and reverse mortgages is essential. They can guide you through the intricacies, help you develop a comprehensive strategy, and ensure your estate plan aligns with your goals and desires.

Case Study: A Real-Life Example

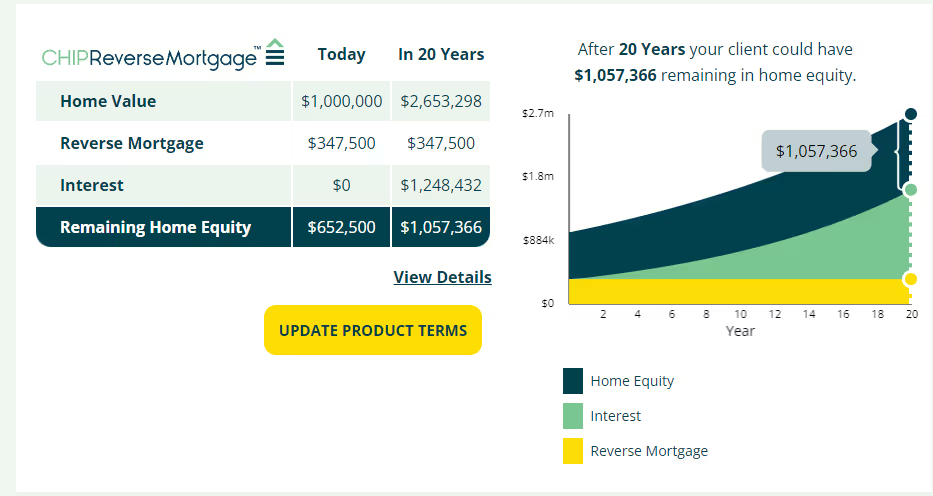

In the example below, our 60-year-old client with a $1,000,000 home was eligible to receive $347,500. This was approximately 35% of the value of the home. After she took her reverse mortgage of $347,500, her remaining home equity was $652,500.

If we assume a 5% property appreciation rate (this is the historical appreciation rate in Canada for the past 20 years), over the next 20 years, her situation would look as follows:

We can see her equity in the home after 20 years would become $1,057,366. In other words, even after enjoying the benefits of a reverse mortgage for 20 years, our client’s equity will increase rather than decrease, and her heirs will not lose any of their inheritance.

This is all happening because even though the reverse mortgage balance is growing over time (the light green line in the chart), so is the overall value of the home (the dark green line in the chart).

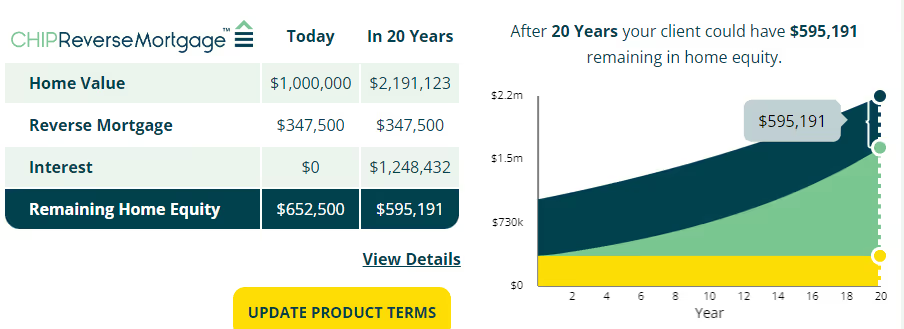

Looking at the chart again, our client’s home equity is the width of the dark green channel. You can see in the chart the green channel is getting wider over the entire 20-year period, meaning her equity is actually growing over time. Even if we were to use a 4% rate of property appreciation (instead of a 5% appreciation rate), the situation for her heirs would still look very good:

In this case we can see our client’s home equity after 20 years will become $595,191. After 20 years of the benefits of a reverse mortgage, the reverse mortgage has only decreased her heirs’ inheritance by $57,309, a change of less than 9%.

Speaking to a knowledgeable, experienced expert in reverse mortgages is key when considering the benefits and consequences of a reverse mortgage.

An advisor can provide you with calculations customized to your personal circumstances and help you feel more comfortable with the entire process. Ultimately, you—and your heirs— should not feel threatened with getting a reverse mortgage.

Maximizing Financial Flexibility

A reverse mortgage can offer you more than just the ability to preserve your inheritance; it also provides financial flexibility and security for both you and your loved ones. Let's explore how:

a) Supplementing retirement income and improving cash flow

Retirement should be a time of relaxation and enjoyment, not constant financial worry. A reverse mortgage allows you to convert a portion of your home equity into tax-free cash, which can be a game-changer for your retirement income.

With this improved cash flow savings every month, you can pursue your passions, travel, spoil your grandchildren, or simply have peace of mind knowing that you have the financial resources to support your desired lifestyle.

b) Paying off high-interest debts to protect your family's financial well-being

By using a reverse mortgage, you can pay off all of your high-interest debts. This frees up cash flow and protects your loved ones from being burdened with these debts after your passing.

c) Accessing funds for healthcare expenses or unexpected emergencies

Life is unpredictable, and unexpected expenses can arise at any moment. Whether it's a medical emergency or home repairs, having access to funds can provide peace of mind.

A reverse mortgage can be a lifeline in these situations, allowing you to tap into your home equity to cover such expenses without depleting your savings or resorting to high-interest loans.

Steps to Protect Your Loved Ones with a Reverse Mortgage

Now that we've highlighted the benefits let's explore the steps you can take to protect your loved ones' inheritance through a reverse mortgage:

a) Conducting thorough research and understanding the terms and conditions

As with any financial decision, educating yourself about reverse mortgages is crucial. Familiarize yourself with the terms, conditions, and obligations involved. By understanding the details, you can make informed choices that align with your goals and desires.

b) Consulting with financial advisors and reverse mortgage specialists

Seeking professional advice is vital when considering a reverse mortgage. Financial advisors and reverse mortgage specialists can provide personalized guidance, ensuring you make decisions that align with your unique financial situation and long-term goals.

They can help you explore different scenarios, assess the impact on your inheritance, and develop a comprehensive estate plan.

c) Developing a comprehensive estate plan to align with your goals and desires.

Integrating a reverse mortgage into your overall estate plan can be prudent. Working with professionals, you can develop a comprehensive strategy that ensures your heirs are well taken care of while allowing you to enjoy the benefits of a reverse mortgage during your lifetime.

A well-crafted estate plan considers various factors, such as tax implications, your desired level of financial support for your heirs, and the preservation of your assets.

Overcoming Common Misconceptions

To fully enjoy the benefits of a reverse mortgage, it's important to dispel the common misconceptions that may cloud your judgment. Let's address some of these concerns and provide clarity:

a) Debunking the myth of losing homeownership.

One common fear is that you will lose ownership of your home by obtaining a reverse mortgage. Rest assured, with a reverse mortgage, you retain full ownership and the right to live in your home for as long as you wish.

The title remains in your name, and you are responsible for maintaining the property, paying property taxes, and keeping up with insurance payments.

b) Explaining the non-recourse feature of reverse mortgages to protect your heirs from debt.

Many homeowners worry about burdening their heirs with debt after their passing. However, reverse mortgages in Canada are non-recourse loans. This means the lender's only recourse for repayment is the home's sale.

Your heirs are not responsible for any shortfall between the loan balance and the home's value. They can choose to retain the home by paying off the loan or sell the property, keeping any remaining equity.

c) With the reverse mortgage balance increasing over time, my equity will disappear

From our case study discussed above, you can see that this is not true. Even though the reverse mortgage balance increases over time, your property value is also increasing.

As long as the reverse mortgage loan amount is kept to a small percentage of the overall home value, “equity loss” for heirs does not typically happen. This is why lenders do not give reverse mortgage loans more than 59% of the home's value. In extreme cases, where property value does not increase, borrowers and heirs remain protected with the “negative equity guarantee” lenders offer.

In our experience, we see most client’s home equity remain the same or increase over time - so heirs almost always receive their inheritance despite the homeowner taking a reverse mortgage. We would describe this as an “equity freeze” rather than an “equity loss”.

The importance of open communication with your loved ones about your financial decisions

From all of our discussions about reverse mortgages, it should become clear that homeowners must have open and honest communications with their family if they are going to get a reverse mortgage.

Discussing your intentions, sharing information about the loan, and addressing any concerns they may have can foster understanding and alleviate anxieties not only for your family but also for yourself.

By involving your family in the decision-making process, you can ensure everyone is on the same page and that your financial choices align with your family's best interests.

Conclusion

In conclusion, reverse mortgages are a powerful tool to protect and enhance your loved one's inheritance. By dispelling misconceptions, understanding the benefits, and taking strategic steps, you can preserve your assets, ensure financial stability for your heirs, and leave a lasting legacy.

Remember to conduct thorough research, seek professional advice, and develop a comprehensive estate plan that aligns with your goals and desires.

If you're ready to explore the possibilities of a reverse mortgage and how it can protect your loved ones' inheritance, we encourage you to reach out to professionals in the field.

Financial advisors and reverse mortgage specialists are equipped to provide personalized guidance and help you navigate this financial journey. You can secure a bright and prosperous future for yourself and your cherished heirs by taking the necessary steps today.