The Canadian reverse mortgage market experienced substantial changes in 2022, with a significant increase in total debt and a notable shift in market share.

According to regulatory filings submitted by Equitable Bank and HomeEquity Bank, total Canadian reverse mortgage debt increased from $4.4 billion to $6.1 billion in 2022, representing an annual increase of 35%.

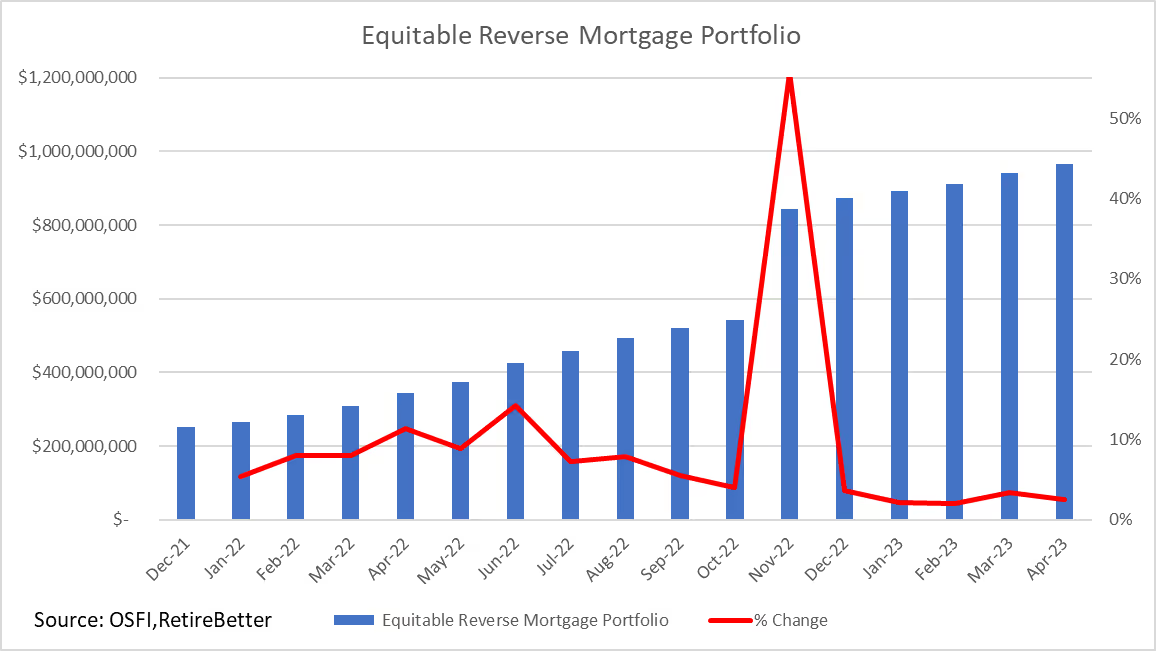

Equitable Bank's Market Surge

2022 was a standout year for Equitable Bank, which more than doubled its share of the Canadian reverse mortgage market, increasing its market share from 6% to 14%.

We attribute this stellar growth by Equitable Bank due to its concerted effort to reach out to its broker partners and promote its products with aggressive compensation levels. Equitable Bank also promoted itself directly to consumers by dropping its pricing for several months.

This strategy significantly impacted the last quarter of 2022 when the bank increased its total portfolio by 40%. This was highlighted by an explosive month-over-month growth of 55% in November 2022.

The growth of Equitable Bank in the reverse mortgage market is a testament to the effectiveness of their direct-to-consumer and partner marketing strategy.

HomeEquity Bank's Steady Growth

While Equitable Bank made headlines with its rapid growth, HomeEquity Bank (HEB) also experienced substantial growth in 2022. HEB grew its portfolio to over $5 billion, representing a year-on-year annual growth of 23%.

This growth demonstrates HEB's continued strength in the reverse mortgage market and its ability to maintain a significant market share despite the aggressive competition.

HEB's growth can be attributed to its long-standing reputation and intensive marketing strategies. The bank has been synonymous with reverse mortgages in Canada, and its CHIP brand is often used interchangeably with reverse mortgages.

The Impact of Market Growth on Consumers

The growth of the reverse mortgage market in 2022 has significant implications for consumers. With more reverse options available than ever, homeowners over the age of 55 have more choices when securing a reverse mortgage.

This increased competition between lenders could lead to a better environment for consumers as they can now actively select the best lender and the best product with the best price.

Mortgage brokers are also becoming more popular with consumers to help them find the best option and to help understand the differences between the Equitable and HEB products.

Looking Ahead

As we move into 2023, it will be interesting to see how this shift in market share impacts the landscape of the reverse mortgage market.

Will HEB follow Equitable Bank's aggressive marketing approach? Will either of the two competitors introduce new products in 2023? If so, how will this affect consumers looking to secure a reverse mortgage?

Furthermore, the strong growth of HEB suggests that there is still room for growth in the reverse mortgage market. As more Canadians reach retirement age, the demand for reverse mortgages will likely continue to grow. Both Equitable Bank and HEB are well-positioned for success.

Summary

The 2022 Canadian reverse mortgage market was a year of significant growth and change. Equitable Bank's aggressive marketing strategy paid off with a substantial increase in market share, while HomeEquity Bank demonstrated steady growth and continued strength in the market.

RetireBetter will continue monitoring these trends and providing insights to help Canadians navigate retirement planning. Stay tuned for more updates on the Canadian reverse mortgage market.