When homeowners over the age of 55 start looking at loan options, they can quickly get overwhelmed with the options.

Many of them then contact us asking us to help them get home equity lines of credit (HELOC).

As we start talking about their needs, we usually ask if they have looked into reverse mortgages…and they usually tell us they know very little about reverse mortgages.

So if you are in the same situation as many of our clients, and are not sure how reverse mortgages work—that’s ok!

Learn more:

Reverse Mortgage Popularity Growing

Having said that, understanding the difference between reverse mortgages and HELOCs in Canada is important as it could make all the difference in your retirement!

While both options offer access to equity in one's home, each product has distinct advantages as well as drawbacks that need careful consideration.

In this article we will look at how these two home equity loans compare and look at the pros and cons of both options— helping you to unlock your potential financial freedom using the equity from your home.

Before we go any further, let’s get some reverse mortgage basics out of the way.

What is a Reverse Mortgage?

Reverse mortgages are a type of home equity loan that is designed for older homeowners to make use of the equity they have built in their homes.

Instead of selling their home, homeowners aged 55 and over can free up funds while still living in their own property.

With a reverse mortgage, a homeowner does not need to make monthly mortgage payments until they sell the home, stop living in it or pass away.

A reverse mortgage loan amount is based on your age, the property’s value and its location.

The older you are, and the more your home is worth, the more your reverse mortgage loan can be.

Your income is not considered by a reverse mortgage lender—which is very important since most seniors are only receiving fixed pension income every month.

Since income and repayment are not very important factors for a reverse mortgage lender, your credit score is also not a factor to qualify for a reverse mortgage loan.

Learn more:

How Does a Reverse Mortgage Work?

With these senior friendly guidelines, reverse mortgages are becoming a popular choice amongst retirees looking to supplement their retirement income or pay off existing debts.

What is a HELOC?

A HELOC is a home equity loan that allows homeowners to borrow money using the home as collateral.

A HELOC is like a credit card because as you borrow money from your HELOC, your available funds go down.

When you pay money back to your HELOC, your available funds go up.

Since your available funds can go “up” or “down” with your usage, a HELOC is also referred to as a “revolving” loan.

HELOCs are very popular with homeowners of all ages because you only pay interest on the amount you borrow. If a HELOC is not used, there is no cost to the homeowner.

As a result, HELOCs are very popular choices for homeowners looking to set up an emergency source of cash.

HELOCs are also a popular option for homeowners who need to finance home renovations, consolidate debt, or pay for other large expenses.

Reverse Mortgages vs. HELOCs: What's the Difference?

At this point, we can see that reverse mortgages and HELOCs are both types of loans that are secured by your home.

However, there are some significant differences between the two.

Repayment Requirements

The biggest difference between reverse mortgages and HELOCs are the repayment terms.

A reverse mortgage does not need to be repaid until the homeowner sells the home, moves out, or passes away. During this time, monthly payments do not need to be made either.

This means that a homeowner could go for years without making payment on the reverse mortgage!

Retired homeowners find this feature very appealing as it significantly improves their monthly cash flow and allows them to manage their affairs in a stress-free manner.

With a HELOC, you are required to make monthly payments on the loan. As long as you keep making your payments, you can keep the HELOC loan in place.

If you do not make the monthly HELOC payments, the payment is added to your HELOC loan balance, reducing your available HELOC credit amount.

If you continue skipping your monthly HELOC payments, you will eventually hit your HELOC credit limit and the bank will require you to start making monthly payments in order to bring the HELOC balance down.

If you do not (or cannot) make these required HELOC payments, the bank could eventually foreclose on your home.

If a retiree makes late payments on the HELOC too many times, they run the risk of hurting their credit rating.

Loan Amounts

With a reverse mortgage, HomeEquity Bank and Equitable Bank will only lend you up to 55% (sometimes 59%) of your home’s appraised value.

These loan limits apply regardless of your age and your property value.

As an aside, if you work with a reverse mortgage broker such as RetireBetter, you can access up to 65% of the value of your home.

With a HELOC, homeowners can access up to 65% of their home’s appraised value—but only if they have sufficient income to qualify for the requested amount.

This income requirement plays a big role in how much retirees can get for a HELOC.

Many retired homeowners with excellent credit will not qualify for a small $30,000 HELOC simply because their only income is CPP or OAS income.

Let’s discuss these income requirements in more detail.

Age Requirements

To qualify for a reverse mortgage, all owners must be at least 55 years old. There is no upper age restriction with a reverse mortgage.

To qualify for a HELOC, a lender will not look at your age, other than to confirm you are at least 18 years old.

Income Requirements

With both CHIP and Equitable Bank, homeowners are not required to show they have enough income to qualify for the loan.

For reverse mortgages, the homeowner only needs to show they have enough income to pay their property taxes and maintain the property. Most retirees are able to satisfy this reverse mortgage income requirement by providing their annual tax documents.

In order to qualify for a HELOC, a lender will look very closely at how much income the homeowner receives—because the homeowner is expected to make monthly payments and eventually pay off the loan.

Most HELOC lenders will only lend 39% - 50% of a borrower’s provable monthly income. The amount of home equity available is not taken into account.

As a simple example, if a retiree has a mortgage free home worth $10 million and receives a total annual pension of $50,000, a lender will only approve them for a HELOC of $19,500 - $25,000.

Credit Requirements

Whether you are looking at CHIP reverse mortgages or any other type of reverse mortgage, your credit score is generally not going to be an issue.

For many seniors who have bad credit, a reverse mortgage can be a life-saver.

Your credit score will be closely reviewed when you apply for a HELOC. A lender will want to make sure you are a low risk borrower and have a history of repaying your debts.

A low score will tell the HELOC lender you are a risky borrower and will often result in your HELOC application being declined.

Loan Proceeds

With a reverse mortgage, most people think you can only receive your funds all at once at the beginning. However, reverse mortgages can be highly customized to fit your needs!

In Canada, you can choose to receive your reverse mortgage funds all at once, in scheduled instalments (like a monthly allowance) or even randomly when you have a need—just like a HELOC!

The advantage of not taking all your reverse mortgage proceeds at the onset is that it reduces your overall interest costs, as you are only charged interest on the money you receive.

With a HELOC, you have complete flexibility on when to receive your funds.

You can choose to borrow your maximum loan amount right from the onset or choose to only use it when you need it. Again, you will only be charged interest when you borrow money.

Lender Options

There are only 2 Canadian Banks that provide reverse mortgages: HomeEquity Bank offers the CHIP Reverse Mortgage and Equitable Bank offers the Flex Reverse Mortgage.

If you work with a reverse mortgage broker, you can get reverse mortgages from smaller regional lenders that are not Canadian Banks.

Learn more:

Using a Mortgage Broker to Get a Reverse Mortgage

Which Lenders Offer Reverse Mortgages

With a HELOC, a homeowner has many options, including all of the national banks and many local credit unions.

Eligible Properties

A reverse mortgage can only be permitted on your primary residence.

Reverse mortgage lenders will not allow you to use a second home (such as cottage) or an investment property as collateral for a reverse mortgage.

A HELOC, on the other hand, is permitted for any type of real estate, regardless of where the homeowner lives.

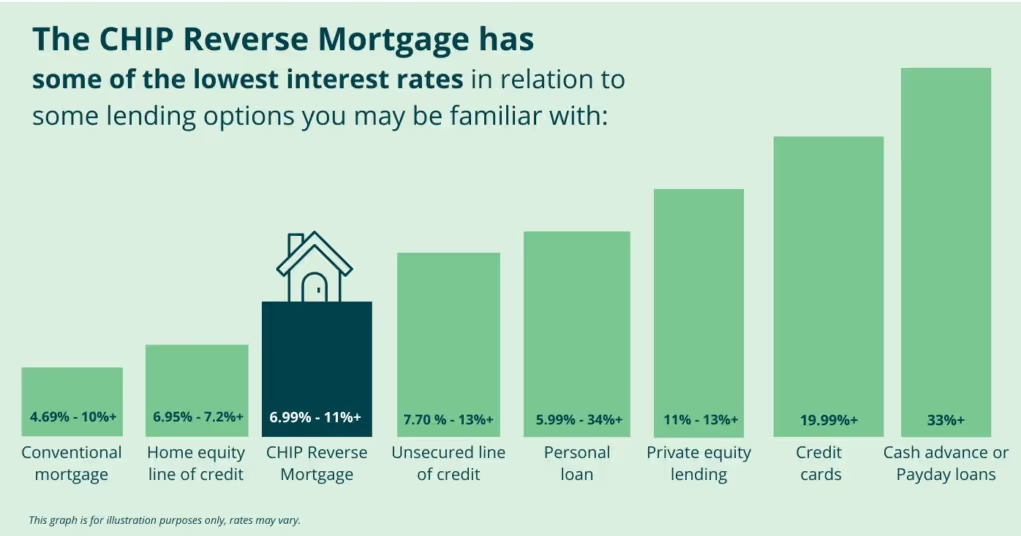

Interest Rates

Most homeowners focus only on the interest rate of a loan when considering their options.

HELOC’s are priced slightly more than traditional mortgages due to their flexible nature but are still on the lower end of the interest rate range for loans.

Depending on your credit and overall circumstances, your HELOC rates may be 1-5% more than traditional mortgage rates.

Reverse mortgages, on the other hand, are approximately 1-3% more than HELOCs since they do not require monthly payments and do not consider your income or credit in order to qualify.

Here is how the interest rates for HELOCs and reverse mortgages compare to each other and various other loan products:

Despite their higher interest rate costs, reverse mortgages are becoming increasingly popular in Canada.

This is happening because retired homeowners are realizing they cannot qualify for their desired HELOC amount or cannot manage the monthly repayments of the HELOC.

Ultimately, these Canadian homeowners are taking a reverse mortgage instead of a HELOC because they are focusing on a higher quality of life with less stress.

Learn more:

Understanding Reverse Mortgage Interest Rates

Which One is Right for You?

The decision between a reverse mortgage and a HELOC will depend on your individual financial situation.

If you are looking for a loan that does not require monthly payments and are comfortable with a slightly higher interest rate, then a reverse mortgage is probably the better choice for you.

On the other hand, if you are looking for a loan that allows you to borrow money as you need it and you are comfortable with making monthly payments, then a HELOC may be the right choice for you.

It's important to note that both products have their advantages and disadvantages, so it's important to focus on your needs and work with an experienced advisor to help you make the process as smooth as possible.

Even if you prefer a HELOC over a reverse mortgage, remember you still need to qualify for the amount you desire!

It's also important to consider the fees associated with each product.

Both reverse mortgages and HELOCs have setup fees associated with them. While not significant, you should be aware of them and factor them into your decision-making process.

Wrapping Up

In conclusion, both reverse mortgages and HELOCs are popular options for homeowners in Canada.

While they may seem similar on the surface, there are some significant differences between the two.

It's important to understand these differences and to do your research before making a decision.

At RetireBetter, we are committed to helping you make an informed decision about your finances.

If you have any questions about reverse mortgages or HELOCs, or if you would like to speak with a financial advisor, please contact us today.