Introduction

As one of Canada’s top reverse mortgage brokerages, we're firm believers in the advantages of reverse mortgages to improve the quality of life for homeowners over the age of 55. In the spirit of openness, let’s address some of the "horror stories" that circulate online about reverse mortgages.

We believe that by discussing these stories about reverse mortgage dangers, we can shed light on the realities of reverse mortgages, dispel reverse mortgage myths, and highlight the benefits that these financial products can offer when used responsibly. Stay tuned as we navigate through these stories, not to scare, but to educate and empower you to make the best decisions for your retirement.

Key Takeaways

- The Canadian reverse mortgage market is dominated by large professionally managed, financially stable, and highly regulated banks compared to the fragmented and regional American market

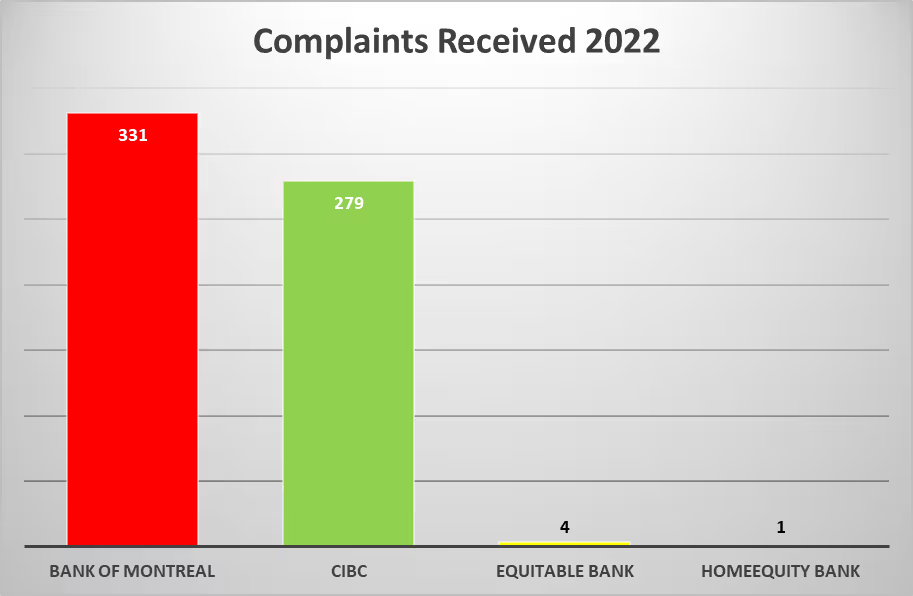

- In 2022, the Ombudsman for Banking Services and Investments received only 1 complaint about HomeEquity Bank and 4 complaints about Equitable Bank.

- If a Canadian homeowner keeps the home insured and in good condition, pays their property taxes and lives in the property, the reverse mortgage will remain in good standing and the lender cannot foreclose on the loan

Some Reverse Mortgage Basics

Before we get into sharing some horror stories with you, let’s quickly give an overview of reverse mortgages. Reverse mortgages allow homeowners aged 55 and older to convert a portion of their home equity into tax-free cash, without having to sell their home or make monthly payments.

The loan is only repaid when the homeowners move or sell the house, or pass away. While reverse mortgages can provide a lifeline for cash-strapped retirees, they also come with responsibilities.

Homeowners must continue to pay property taxes, homeowner's insurance, and maintain their home in good condition. They must also live in the property as their primary residence.

If you want to learn more about reverse mortgages, we’ve written some useful articles you can read:

- How Does a Reverse Mortgage Work in Canada?

- Can a Homeowner with Bad Credit Get a Reverse Mortgage?

- The Difference Between a Reverse Mortgage and a HELOC

- What Your Obligations with a Reverse Mortgage?

Now that we’ve covered the basics about reverse mortgages, let’s look at some of the reverse mortgage horror stories that have made headlines.

We'll discuss what went wrong, how these situations could have been avoided, and how, contrary to what these stories might suggest, reverse mortgages can indeed be a great solution for many homeowners.

The Dark Side of Reverse Mortgages: A Closer Look

It's important to note that many (all?) of the horror stories circulating online originate from the United States, where the reverse mortgage market operates differently than in Canada. But these are the stories circulating so we decided to use them for our discussion.

Let's examine several of these stories:

Story 1: The Case of the Misidentified House

In Alabama, NBC 15 News reported about Charlotte Kirby, an elderly woman who faced foreclosure on her home because her reverse mortgage lender mistakenly inspected a vacant restaurant next door and deemed her house unoccupied.

This is an extremely unusual situation and resulted from the lender's negligence rather than the nature of the reverse mortgage itself. The woman eventually received significant compensation in court.

Comment on its likelihood in Canada

In Canada, such a situation is almost impossible as reverse mortgages are provided by 2 highly respected and ethical lenders, namely HomeEquity Bank and Equitable Bank.

Both reverse mortgage lenders are subject to a highly regulated industry with oversight by the Office of the Superintendent of Financial Institutions and each has robust complaint resolution processes.

While any bank can make mistakes, it’s highly unlikely these banks could commit such negligence.

Story 2: The Case of the Marshall Fire Victim

In Colorado, CBS News reported about an 80-year-old man named Ed Sharp who lost his home in a large natural fire and was living elsewhere while he waited for his home to be rebuilt.

Despite this, Sharp’s reverse mortgage company began to foreclose on the reverse mortgage since the property was no longer his primary residence. After intervention from a local representative, the mortgage company rescinded the foreclosure.

Comment on its likelihood in Canada

In Canada, such a situation is unlikely due to the protections in place for homeowners. Canadian lenders are typically willing to work with homeowners facing difficulties to avoid foreclosure. Additionally, there are disaster relief programs and insurance coverages that can help homeowners in the aftermath of natural disasters.

However, this story underscores the importance of maintaining open communication with your lender, especially in the face of unforeseen circumstances. Let's move on to the third story.

Story 3: The Case of the Fraudulent Contractor

The Naples Daily News reported about Gerda Graf who reportedly lost her home after defaulting on a reverse mortgage. She took out the mortgage to cover the cost of home renovations, but a fraudulent contractor vanished with the money.

Subsequently, she fell ill and was unable to keep up with her home insurance premiums, property taxes, and homeowner’s association fees. Her reverse mortgage went into default, and she lost her home.

Comment on its likelihood in Canada

While unfortunate, this situation is really about the importance of due diligence when hiring contractors. In Canada, homeowners have access to numerous resources to verify the credibility of contractors.

Additionally, Canadian lenders are typically willing to work with homeowners facing difficulties to avoid foreclosure. Certainly the laws of foreclosure in Canada are different than those in the United States and permit the homeowner to fix any default prior to the home being taken over by the bank.

Are Canadian Reverse Mortgage Lenders Predatory?

After dealing with both HomeEquity Bank and Equitable Bank over a number of years, we certainly do not think they are predatory. Still, we were curious how their customers felt about them; are industry regulators receiving complaints about reverse mortgages?

We researched the Annual 2022 Report from the Ombudsman for Banking Services and Investments to see how many complaints the industry ombudsman received about these banks last year. We compared the reverse mortgage lender complaints with 2 prominent Canadian banks to provide additional context:

Based on the number of complaints their own clients filed with OBFI last year, you can see that these reverse mortgage lenders are not upsetting their clients. From this, we can reasonably conclude that these lenders are not creating “horror stories” for their clients either.

A Stable & Ethical Reverse Mortgage Market in Canada

In Canada, reverse mortgages come with built-in protections and are offered by stable and ethical lenders. As discussed in a World Economic Forum report, Canada's banking system is robust and diversified, unlike the fragmented situation in the United States where smaller lenders seem to act recklessly.

Moreover, Canadian lenders are required to be transparent about fees, and there are only two reverse mortgage lenders: HomeEquity Bank and Equitable Bank. This lack of competition reduces the likelihood of predatory lending practices.

In fact, reverse mortgages in Canada come with a guarantee that as long as borrowers keep up with their obligations, they will never end up owing more than their home is worth. This is a significant safeguard that protects Canadian homeowners and their heirs.

In the next section, we'll discuss the myths and realities of reverse mortgages, providing you with the information you need to make informed decisions about your financial future.

Debunking Common Myths About Reverse Mortgages

As with any financial product, reverse mortgages are often surrounded by myths and misconceptions. We’ve debunked common misconceptions about reverse mortgages before but let's debunk some of the most common myths here:

Myth 1: The Bank Owns Your Home

Contrary to popular belief, when you take out a reverse mortgage, you keep ownership of your home.

The bank only takes ownership if you default on the loan, which is rare and difficult, especially in Canada where lenders work closely with homeowners to avoid this outcome.

In our experience, Canadian banks will go out of their way to accommodate homeowners before enforcing on a mortgage—they really do not want to deal with owning your home.

Myth 2: You Will End Up Owing More Than Your Home is Worth

In Canada, reverse mortgages come with a "no negative equity guarantee." This means that as long as you meet your obligations (such as paying property taxes and maintaining insurance), you'll never owe more than your home is worth.

In fact, according to HomeEquity Bank, more than 95% of CHIP reverse mortgage borrowers end up having remaining equity after they sell their home and pay off the loan.

Myth 3: Reverse Mortgages Are a Nightmare for Heirs

Many people worry that a reverse mortgage will leave their heirs with a financial mess. However, in our experience, almost all reverse mortgages are paid off in a smooth, organized manner with sufficient time being given to the heirs to complete the process.

On this last point, both of the major Canadian reverse mortgage lenders allow up to 6 months for the loan to be repaid by the borrower’s heirs after it comes due.

In terms of remaining equity, due to the conservative lending habits of Canadian reverse mortgage lenders and the robust Canadian real estate market, almost all loans are paid off with the heirs receiving a substantial inheritance.

Moreover, heirs have several options to settle the loan, including selling the home or paying off the loan with other funds to retain ownership of the property. Overall, a reverse mortgage can be paid off without causing nightmares for your heirs.

The Benefits of Reverse Mortgages

Despite these sensationalistic horror stories, in our experience of arranging reverse mortgages since 2016, we find them to be an excellent tool for many homeowners.

With a reverse mortgage, retired homeowners can access the equity in their home without selling it or making monthly mortgage payments, providing a source of income during retirement.

They can be used to cover living expenses, pay off debts, help with healthcare costs, or even fund home renovations or vacations. Funds can be received lump sum or in installments.

Reverse mortgages can also provide financial relief and flexibility. Since the money received from a reverse mortgage is tax-free, it won't affect Old-Age Security or Guaranteed Income Supplement payments.

Want to learn more about the benefits of reverse mortgages? Check out this article:

Alternatives to Reverse Mortgages

While reverse mortgages can be a great solution for many, it's important to consider all your options. Other alternatives might include downsizing to a smaller home, renting out a portion of your home, or exploring traditional mortgage or lines of credit options. Each of these alternatives has its own pros and cons, and the best choice depends on your individual circumstances and goals.

You can learn more here:

- Reverse Mortgages vs Home Equity Loans?

- Pros and Cons of Downsizing for Seniors

- Pros and Cons of Reverse Mortages

Making the Right Decision

At RetireBetter.ca, we believe in the power of reverse mortgages as a financial tool, but we also understand that they're not for everyone. It's essential to consider your personal circumstances, financial needs, and long-term goals before deciding.

We're here to provide you with all the information you need to make an informed decision. If you're considering a reverse mortgage, we encourage you to reach out to our team of experts.

We're committed to helping Canadian homeowners navigate their retirement years with confidence and financial security. In the end, the key to avoiding a reverse mortgage horror story is education and understanding how the product works.

By knowing the facts, asking the right questions, and working with a reputable lender, you can use a reverse mortgage to enhance your retirement and live better.

Want to see answers to your reverse mortgage questions? Check out our Reverse Mortgages FAQs.

Learn more:

CHIP Reverse Mortgage vs Equitable Bank's Reverse Mortgage

Wrapping Up

Reverse mortgages can be a powerful tool for homeowners looking to enhance their retirement years. While the horror stories circulating online can be alarming, it's important to remember that these represent the exception, not the rule. In Canada, reverse mortgages come with numerous safeguards and are offered by reputable lenders committed to ethical practices.

At RetireBetter.ca, we're dedicated to helping Canadian homeowners navigate the complexities of reverse mortgages.

We believe in the power of education and transparency, and we're here to provide you with the information you need to make informed decisions about your financial future.

Remember, a reverse mortgage can be a great way to tap into your home's equity and enjoy a more comfortable retirement. But as with any financial product, it's essential to understand the terms, conditions, and obligations before signing on the dotted line.

FAQ

- Can my lender force me to sell if I satisfy all of my obligations under my reverse mortgage?

If you obtain your reverse mortgage from one of the national lenders in Canada, and meet all of your loan obligations, you can live in your home for life without having to repay your reverse mortgage loan.

- If I travel frequently or live abroad during the winter months, will my lender be able to foreclose on my reverse mortgage?

You are required to live in your home for at least 6 months of the year in order for it to be considered your primary residence; if you meet this requirement, you have satisfied the loan requirement to keep living in the home.

- Can my reverse mortgage lender pay my property taxes for me like my regular mortgage lender did?

No, HomeEquity Bank and Equitable Bank do not manage property tax payments for their reverse mortgages. Homeowners are responsible to pay their property taxes themselves and may be required to provide proof of payment to the lenders if requested.