Introduction

In the world of home financing, reverse mortgages have emerged as a popular way for homeowners looking to tap into their home equity without selling their property.

However, like any financial product, it's crucial to understand how a reverse mortgage works. One of the key aspects to consider is the interest rate, which can significantly impact the cost of a reverse mortgage over time.

In this article, we’ll look at the role of interest rates on reverse mortgages and how they compare to regular mortgage rates in Canada.

Key Takeaways

- Rising interest rates in Canada will result in higher reverse mortgage interest rates and smaller loan amounts.

- Rising interest rates will also lower the demand for reverse mortgages.

Understanding Reverse Mortgages

Definition and Purpose of Reverse Mortgages

A reverse mortgage is a loan that allows homeowners, over the age of 55 years, to convert some of the equity in their homes into cash.

Unlike a traditional mortgage, where the homeowner makes regular payments to the lender, a reverse mortgage requires no monthly payments. Instead, the loan, along with the accumulated interest, is repaid when the homeowner sells the house, moves out permanently, or passes away. The main purpose of a reverse mortgage is to provide financial flexibility to homeowners, especially those on a fixed income.

It can be used to cover living expenses, pay off existing debts, fund home improvements, or even as a financial tool for estate planning. Homeowners can receive funds lump sum or set up a line of credit.

To learn more about reverse mortgages, you can read the following:

Repayment of Reverse Mortgages

The repayment of a reverse mortgage is unique and differs significantly from a traditional mortgage. With a traditional mortgage, the homeowner makes regular payments to gradually reduce the loan balance.

However, with a reverse mortgage, the loan balance increases over time as interest accumulates. A homeowner is only required to repay the loan, along with the accumulated interest, when the homeowner sells the house, moves out permanently, or passes away.

It's important to note that the homeowner can never owe more than the fair market value of their home, thanks to the "non-recourse" feature of reverse mortgages in Canada. This feature ensures that the loan amount does not become a burden to the homeowner or their heirs.

If you want to learn more about repaying a reverse mortgage, you can read the following guide:

The Role of Interest Rates in Reverse Mortgages

Interest Rates Influence Loan Cost

Interest rates play a crucial role in determining the borrowing cost of a reverse mortgage.

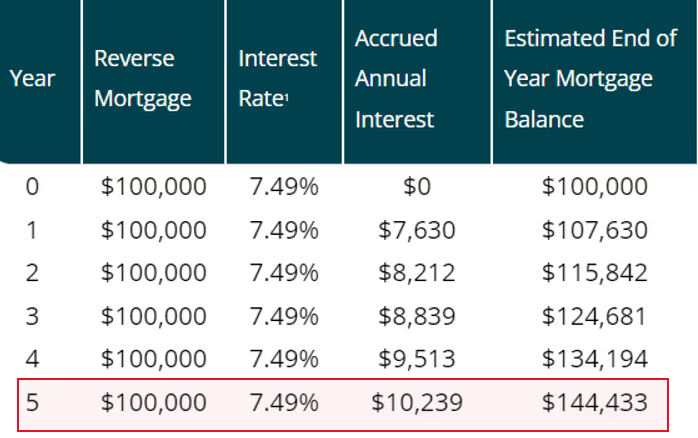

A reverse mortgage with an interest rate of 7.49% would accumulate interest in 5 years as follows:

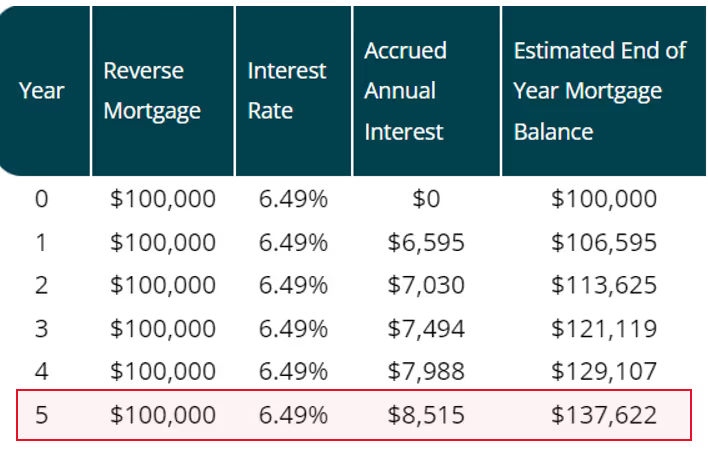

If we were to reduce the interest rate by 1% to 6.49%, then after 5 years, the reverse mortgage interest costs would look like this:

From the above diagrams, we can see that a 1% difference for a $100,000 reverse mortgage will cost a homeowner $6,811 in additional interest costs after 5 years.

While we do not believe a homeowner should avoid a reverse mortgage because of interest costs alone, it is important to understand how interest rates affect the overall cost of borrowing.

Impact of Interest Rates on Loan Amount

Interest rates can also affect the amount that a homeowner can borrow with a reverse mortgage. Lenders use a calculation that takes into account the homeowner's age, the appraised value of the home, and the current interest rate to determine the maximum loan amount.

As a general rule, the lower the interest rate, the more a homeowner can borrow. This happens because with a lower interest rate, the reverse mortgage balance will grow slower over time and the lender will be able to approve a larger loan amount without exceeding its internal loan-to-value restrictions.

Factors Influencing Reverse Mortgage Interest Rates

The Benchmark Interest Rate

The Bank of Canada's benchmark interest rate is a key factor that influences reverse mortgage rates. When the benchmark rate changes, both traditional mortgage and reverse mortgage rates will change in the same direction.

For example, when the Bank of Canada lowered the benchmark rate to near zero in response to the COVID-19 pandemic, mortgage rates, including reverse mortgage rates, also fell.

Market Conditions

Market conditions, such as inflation and economic growth, can also affect reverse mortgage rates. For example, in a strong economy with high inflation, the Bank of Canada might raise the benchmark interest rate to control inflation.

This will lead to an increase in both regular and reverse mortgage rates. We have been seeing this exact scenario unfold recently: the Bank of Canada has been steadily increasing its benchmark rate in 2023 and we have seen traditional mortgage and reverse mortgage rates increase.

Lender's Risk Assessment

Lenders also set their reverse mortgage interest rates based on their own assessment of overall risk. If lenders are concerned about their overall risk exposure, then they will increase their lending rates accordingly.

Fixed vs. Variable Rates in Reverse Mortgages

Definition and Differences

Both regular mortgages and reverse mortgages can have fixed or variable rates. A fixed rate stays the same for the term of the loan, while a variable rate can change based on market conditions. Based on overall market conditions and their own internal risk assessments, reverse mortgage lenders can set their fixed and variable interest rates at different levels.

Here is an example of how a lender can offer different interest rates for different mortgage terms, as well as fixed and variable interest rates:

From the above chart, you can see how the lender is offering a much higher variable rate (for a 5 year term) in comparison to fixed rate terms.

The lender is offering these rates based on a Bank of Canada benchmark rate that is currently high as well as market projections that interest rates will fall over the next few years.

Impact on the Cost of the Loan

We know that different interest rates can make a difference to the long-term borrowing costs of a reverse mortgage. Similarly, when we see differences between fixed and variable rates, the decision to take a fixed interest rate over a variable rate can also have a significant impact on the borrowing costs of a reverse mortgage.

Choosing the right option depends on the homeowner's financial situation and risk tolerance. It's important to carefully consider these factors and consult with a financial advisor or mortgage professional before deciding.

Comparing Regular Mortgage and Reverse Mortgage Interest Rates

When comparing reverse mortgage rates with regular mortgage rates, it's important to note that reverse mortgage rates are typically higher. This is primarily due to the increased risk that lenders take on with a reverse mortgage.

Unlike a regular mortgage, where the borrower makes regular payments to gradually reduce the loan balance, a reverse mortgage does not require any payments until the homeowner sells their home, moves out, or passes away.

According to a report from the Canadian Association of Accredited Mortgage Professionals, the average interest rate for a reverse mortgage in Canada is typically 1-2% higher than for a regular mortgage.

Impact of Interest Rates on Reverse Mortgage Demand

From our discussion, we know that reverse mortgage interest rates are dependent on the Bank of Canada’s benchmark rate, overall market conditions, and the lender’s risk profile and are typically 1-2% points higher than a regular mortgage.

So what happens to reverse mortgage demand when we are in a rising interest rate environment?

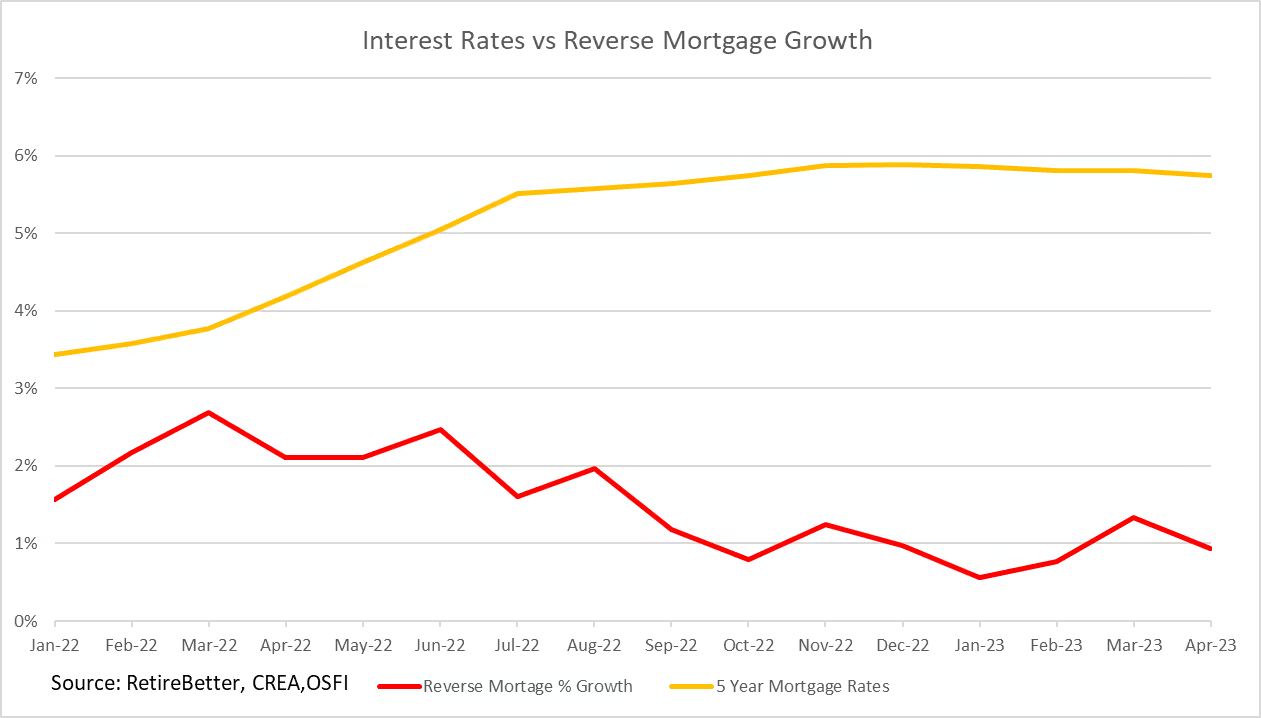

From the above chart, you can see how as interest rates have been steadily increasing since January 2022, we have seen a steady drop in the growth rate of reverse mortgages sold by HomeEquity Bank and Equitable Bank.

While homeowners are still taking reverse mortgages in record numbers, the trend is clear: fewer people are taking reverse mortgages as interest rates (for both regular and reverse mortgages) rise.

This trend mirrors the earlier trend we witnessed, when interest rates were much lower and reverse mortgage demand was booming to record levels.

Navigating Interest Rates When Choosing a Reverse Mortgage

Importance of Considering Fixed or Variable Interest Rates

When choosing a reverse mortgage, it's important to consider the interest rate, as it will significantly impact the cost of the loan over time. A lower rate means less interest will accumulate, reducing the overall cost of the loan.

Therefore, it's important to compare different fixed and variable rate offers and consider both the current rate and the potential for rate changes in the future.

Comparing Different Lenders

Different lenders will offer different interest rates for reverse mortgages. Some may offer fixed rates, while others may offer variable rates.

Even if they both offer fixed rates, they will often offer the same term for different fixed rates. When comparing different offers, consider both the rate and the type of rate (fixed or variable). Also, consider other factors such as fees and loan terms.

Seeking Professional Advice

Given that most homeowners are not familiar with reverse mortgages and the importance of interest rates, it's advisable to consult a professional specializing in reverse mortgages.

They can provide personalized advice based on your financial situation and help you understand a reverse mortgage's potential costs and benefits.

Summary

Understanding the impact of interest rates on reverse mortgages is crucial for any homeowner considering this type of loan. Interest rates can significantly affect the cost of the reverse mortgage loan and the amount that can be borrowed.

Rising interest rates in Canada will result in higher reverse mortgage interest rates and lower approval amounts. Rising interest rates will also lower the demand for reverse mortgages.

Therefore, it's important to carefully consider the interest rate, compare different offers, and seek professional advice. With careful planning and consideration, a reverse mortgage can be a valuable financial tool for homeowners.