For many retirees who are looking to improve their financial situation, a common solution is to tap into the equity of their homes.

When these retirees contact us to discuss how to access their home equity, they typically ask for information about obtaining a home equity line of credit.

Yet, after discussing their retirement needs and income, we find many of these retirees end up taking a reverse mortgage instead.

Why is that?

In this blog post, we explore reverse mortgages and home equity loans, their advantages and disadvantages and the factors a retired homeowner should be aware of when considering either option.

Let’s start with a quick discussion about reverse mortgages.

What is a reverse mortgage?

A reverse mortgage is a special type of mortgage designed for older homeowners who have lots of equity in their home but have limited income.

With a reverse mortgage, retired homeowners can exchange their home equity for cash without having to sell their home, which is normally what a homeowner would need to do in order to access the value of their home equity.

After getting a reverse mortgage, retirees can live in their home for life without having to make any monthly payments.

Learn more:

Unlocking the Benefits of Reverse Mortgages

Can You Get a Reverse Mortgage with Bad Credit?

How Does a Reverse Mortgage Work?

Unlike traditional mortgages that look at your income, your credit history and your repayment ability in order to qualify, reverse mortgages focus on your age and the value of your home.

The older you are and the more your home is worth, the larger your reverse mortgage approval will be.

Instead of a borrower making monthly payments and slowly paying off the loan balance, with a reverse mortgage, the interest is added to the original loan amount.

The reverse mortgage lender will not get repaid until the borrower sells the home, moves out or passes away.

Learn more:

How Does a Reverse Mortgage Work in Canada?

Reverse Mortgage Eligibility Criteria

In order to qualify for a reverse mortgage in Canada, you must meet the following criteria:

- You must be at least 55 years of age.

- You must have at least 45% equity in your home.

- You can only use the reverse mortgage for your principal residence

- Your home must be worth at least $100,000.

Learn more:

What are the Age Rules for a Reverse Mortgage?

Retirees can see how much of a reverse mortgage they qualify for by using RetireBetter’s online reverse mortgage calculator.

Learn more:

The Best Online Reverse Mortgage Calculators

The Danger of Using Google’s Top Ranked Reverse Mortgage Calculators

Which Lenders Offer Reverse Mortgages?

In Canada, there are only 2 banks that offer reverse mortgages: HomeEquity Bank offers the CHIP Reverse Mortgage and Equitable Bank offers the Flex Reverse Mortgage.

Having said that, mortgage brokers that specialize in reverse mortgages, such as RetireBetter, do have access to smaller, regional lenders that also offer reverse mortgages.

These alternative reverse mortgage lenders can be useful if you are a homeowner who is not able to qualify for a large enough reverse mortgage from either HomeEquity Bank or Equitable Bank.

The large 5 banks in Canada do not offer reverse mortgages. If you ask your branch about a reverse mortgage, they will refer you to HomeEquity Bank which has referral partnerships with all of the major 5 banks.

Learn more:

Which Lenders Offer Reverse Mortgages in Canada?

Types of Reverse Mortgages in Canada

You can get 2 different types of reverse mortgages in Canada.

The first type of reverse mortgage gives you all of the money as a lump-sum payment and you start paying interest on the entire amount from the date of advance.

The second type of reverse mortgage is very similar to a home equity line of credit: you can borrow from it as you need the money and you only pay interest on the funds you borrow.

This second type of reverse mortgage can also be set up to give you scheduled advances of funds, and many homeowners over the age of 55 use it to supplement their monthly CPP or OAS pension income.

The lump sum reverse mortgage is available in both fixed and variable interest rates for terms from 6 months to 5 years.

The reverse mortgage that acts like a line of credit is only available in variable interest rates for a term of 6 months to 5 years.

Learn more:

Supplement Your Pensions with a Reverse Mortgage

Reverse Mortgage Advantages and Disadvantages

Like any financial product, reverse mortgages have their advantages and disadvantages.

Here is a brief summary of the advantages of a reverse mortgage:

Advantages

- No regular loan payments are required

- Very easy credit and income requirements to satisfy

- Funds can be used for any purpose, including renovations or to age-in-place

- You stay as the owner of your home for life

- Funds are received tax-free and do not affect your government pensions

You must be wondering, what are the disadvantages of getting a reverse mortgage? Why do people traditionally feel so strongly against getting a reverse mortgage?

While we believe reverse mortgages have a bad reputation due to experiences in other countries (where different rules apply) or lack of familiarity, there are some elements about reverse mortgages that should be considered:

Disadvantages

- Reverse mortgages have slightly higher interest rates than conventional mortgages.

- Your home equity can be reduced over time.

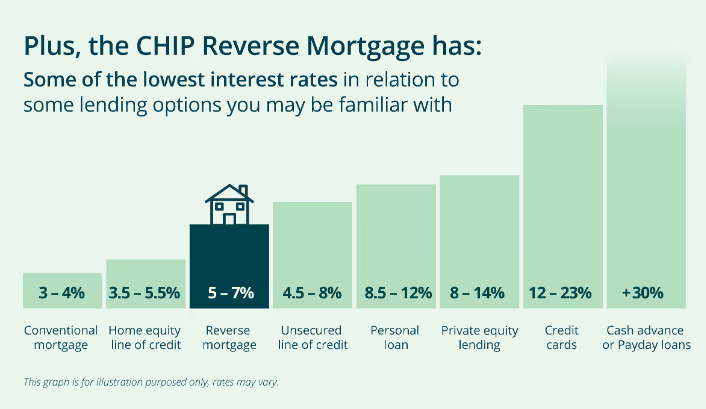

While it’s true that reverse mortgage interest rates are higher than conventional mortgages and traditional home equity lines of credit, they are not as high as people believe.

In fact, reverse mortgage interest rates tend to fall in the middle of loan options: they are more than traditional mortgages/lines of credit but far less than interest rates for personal loans, private mortgages, alternative mortgages and credit cards.

In the following chart, you can see how the CHIP Reverse Mortgage interest rates compare to interest rates of other, more common loan options. Note, the Equitable Bank interest rates are similar to the CHIP Reverse Mortgage interest rates.

Learn more:

How is Reverse Mortgage Interest Calculated?

As for all the reverse mortgage horror stories that make the rounds, we’ve debunked them before. The reverse mortgage environment in Canada is very different from the reverse mortgage market in the United States and the customer satisfaction levels with HomeEquity Bank and Equitable Bank are far superior to those experienced at the regular banks.

Learn more:

Reverse Mortgage Horror Stories Debunked

What is a Home Equity Loan?

A home equity loan is any type of loan where a homeowner borrows against the value of their home. The most common types of home equity loans are mortgages and home equity lines of credit.

Regardless of which type of home equity loan a homeowner gets, the lender requires monthly repayments to be made.

How Does a Home Equity Loan Work?

When a homeowner applies for a home equity loan, the loan approval will be based on the homeowners income level, their credit history and the value of their home.

The more income you have and the more valuable your home, the more you will be approved for.

Between these two factors though, a lender will primarily focus on a homeowner’s income level.

Even if you have a mortgage free home, a home equity loan amount will be based on the borrower’s ability to make monthly payments.

For seniors, this focus on income can be a surprise when they are declined for a home equity line of credit even though their home is mortgage free. Unfortunately, the application is declined because of limited income in retirement.

Home Equity Loan Eligibility Criteria

The eligibility criteria for home equity loans are far more strict than those for a reverse mortgage.

In order to qualify for a home equity loan in Canada, you must meet the following criteria:

- The monthly loan repayment cannot be more than 39%-50% of your monthly income

- You must be at least 18 years old

- You must have at least 15% equity in your home.

- Your credit score must be over 600

Note there is no maximum age to get a home equity loan. Lenders will provide a home equity loan to seniors of any age, so long as their monthly income is enough to make the required repayments.

Learn more:

Which Lenders Offer Home Equity Loans?

All of the 5 major banks and local credit unions in Canada offer home equity loans. Equitable Bank offers both home equity loans as well as reverse mortgages.

HomeEquity Bank does not offer traditional home equity loans.

Types of Home Equity Loans

There are 2 options for homeowners in Canada who are looking to get a home equity loan: a line of credit or a mortgage.

When applying for home equity lines of credit (commonly known as HELOCs), a borrower will only pay interest on the money they borrow.

With a mortgage, the homeowner will receive all of the funds at once and will start paying interest on the entire loan amount from the date of advance.

HELOCs are typically offered with variable interest rates and mortgages can be offered with both fixed or variable interest rates. Borrowers can obtain both types of home equity loans for terms that range from 1-5 years.

Home Equity Loan Advantages and Disadvantages

Home equity loans provide a familiar solution for homeowners wishing to borrow against their home equity.

Here are the advantages and disadvantages of home equity loans, specifically for the homeowners who are over the age of 55:

Advantages

- Funds can be used for any purpose, including renovations or to age-in-place

- Lowest interest rates offered

- Funds are received tax-free and do not affect your government pensions

- Your home equity will not be reduced over time

- Can be used on primary residence or any other real estate

Disadvantages

- Monthly payments of principal and interest required

- Good credit and minimum income required

- You could lose your home if the loan goes into default

Learn more:

Why You Should Use a Mortgage Broker to Get a Reverse Mortgage

The Guide to Using a Mortgage Broker in Canada

When a Reverse Mortgage is Better than a Home Equity Loan

A reverse mortgage and a home equity loan are both reasonable ways for older homeowners to tap into the equity in their home.

However, in our experience, there are certain situations where a reverse mortgage is a better option than a home equity loan:

- You are having monthly cash flow issues

- You are retired and have a mortgage

- You don’t want to move into a retirement home

- You have limited family support

- You want to give family members an early inheritance

- Your health care costs are rising

- You have a private mortgage in retirement

Learn more:

15 Signs It’s Time to Get a Reverse Mortgage

Key Take-Aways

- Reverse mortgage qualification is based on the homeowner’s age and property value while home equity loan qualification is based on income and ability to repay the loan

- A reverse mortgage is a lifestyle product designed to improve the cash flow and lifestyle for homeowners over the age of 55 while a home equity loan is a loan product meant for borrowers of any age

- Home equity loans can be obtained from most banks and credit unions while reverse mortgages can only be obtained from 2 banks in Canada

Wrapping Up

Deciding between a reverse mortgage and a home equity loan can be a big decision - but with the proper guidance, you can be comfortable knowing you are going to make the right decision.

We strongly suggest you focus on your lifestyle needs and speak with a mortgage broker who specializes in reverse mortgages before you make any decision about getting a home equity loan or a reverse mortgage..

Not only will a reverse mortgage specialist be able to give you accurate information about reverse mortgages, but they will also be able to offer you a home equity loan if that is truly the best option for you.